Your company just became uninsurable for the very technology your board approved last quarter. The insurance industry knows something you don’t.

The Great Risk Transfer Illusion

For decades, corporate risk management operated on a simple premise: deploy, insure, repeat. Whatever harm your products or services might cause, there was always a policy to absorb the blow. This assumption became so deeply embedded in business strategy that it functionally disappeared from conscious thought—like oxygen, always there until suddenly it isn’t.

In January 2025, the oxygen ran out.

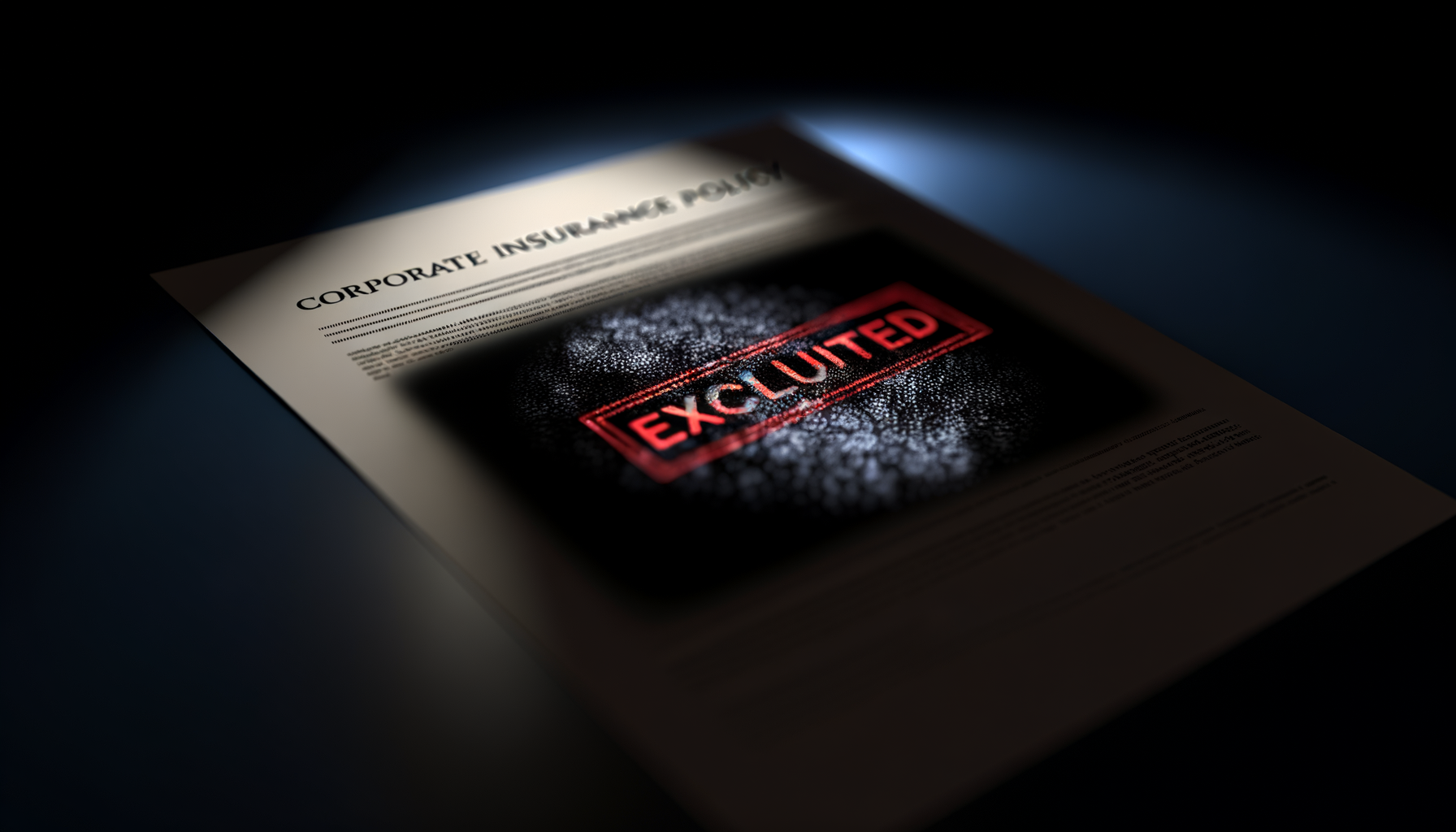

According to the latest AI insurance market analysis, insurers began adding broad generative AI exclusions to errors and omissions (E&O) and media liability policies at their 1/1 2025 renewals. Not narrow carve-outs. Not increased premiums. Wholesale exclusions that leave companies exposed to the very risks their AI deployments create.

Meanwhile, 78% of organizations now use AI in at least one business function. The math here is brutal: three-quarters of businesses have baked AI into their operations while the insurance industry is methodically removing the safety net beneath them.

We’ve built an entire AI economy on the assumption that someone else will pay when things go wrong. The insurance industry just answered: they won’t.

This isn’t hyperbole. This is actuarial reality catching up with technological ambition. And the implications for corporate accountability are more profound than most executives realize.

Inside the Insurance Industry’s AI Reckoning

To understand why insurers are retreating, you need to understand how insurance actually works. Underwriters price risk based on historical data, predictable loss patterns, and actuarial models refined over decades. AI—particularly generative AI—breaks every single one of these mechanisms.

The Unknowable Risk Problem

Traditional software follows deterministic paths. Input A produces output B. When something goes wrong, you can trace the failure, assign responsibility, and quantify damages. Insurance models can handle this.

Generative AI operates differently. Large language models produce outputs that even their creators cannot fully predict or explain. When an AI system generates harmful content, provides dangerous advice, or makes a discriminatory decision, the chain of causation becomes extraordinarily difficult to establish. Was it the training data? The model architecture? The deployment context? The prompt engineering? The user interaction?

Legal analysis of AI-generated content liability reveals the core question insurers cannot answer: who is legally responsible when no human is directly involved in creating the harm? Without clear liability assignment, underwriting becomes guesswork—and insurers don’t stay in business by guessing.

The Aggregation Nightmare

Here’s what keeps insurance executives awake at night: correlated losses.

When a single AI model—say, one of the major foundation models used by thousands of companies—produces systematic errors, every organization using that model faces liability simultaneously. Unlike car accidents or property damage, which occur independently, AI failures can cascade across entire industries in hours.

Imagine a foundation model hallucinates medical information. Suddenly, every healthcare app, customer service bot, and clinical decision support tool using that model becomes a liability. Every insurer covering those applications faces claims simultaneously. This is not a theoretical risk—over 50 class action lawsuits already allege “AI washing,” where companies misrepresented their AI capabilities. These cases are reshaping how underwriters view D&O, E&O, and cyber coverage.

The Moral Hazard Amplifier

Insurance creates moral hazard: when you’re protected from consequences, you take more risks. Insurers manage this through deductibles, exclusions, and premium adjustments. But AI amplifies moral hazard in ways traditional controls cannot address.

Research on the limits of AI regulation through liability and insurance highlights a fundamental problem: companies racing to deploy AI often lack the governance structures to manage the risks they’re creating. Only 1% of organizations have achieved mature AI integration with proper governance, yet 78% are deploying AI anyway. From an insurer’s perspective, this is like selling fire insurance to people actively playing with matches in gasoline-soaked buildings.

The Paradox Takes Shape

Now the paradox becomes clear. The AI liability insurance market is projected to reach $4.8 billion by 2032, growing at approximately 80% CAGR. That’s explosive growth. But this growth is happening in specialized products, on insurers’ terms, with tighter wording and targeted coverage.

Standard policies are adding exclusions. Specialized policies are emerging but with strict requirements most companies cannot meet. The gap between AI deployment and insurable AI deployment is widening, not closing.

Nine in ten businesses express interest in insurance for GenAI risks. But interest doesn’t translate to coverage when the coverage comes with requirements most organizations can’t satisfy.

The emerging AI-specific insurance products require:

- Documented governance frameworks with board-level oversight

- Formal AI risk assessment processes

- Human oversight mechanisms for high-risk decisions

- Bias testing and fairness audits

- Incident response plans specific to AI failures

- Contractual clarity on AI vendor liability

Remember that 1% maturity statistic? That’s roughly the percentage of organizations that can actually meet these requirements. Everyone else is deploying AI while effectively self-insuring against its harms.

The Legal Walls Closing In

While insurance coverage retreats, legal liability expands. This is the worst possible combination for corporate risk managers.

The 2025 State Law Explosion

Analysis of 2025 state AI laws reveals a rapidly expanding liability landscape. States are moving aggressively on AI regulation, and the penalties are substantial:

| Jurisdiction/Law | Focus Area | Potential Penalties |

|---|---|---|

| Colorado AI Act | High-risk AI systems | Up to $250,000 per violation |

| Illinois AI Therapy Regulation | AI in mental health | $10,000 per violation |

| Various State Deepfake Laws | AI-generated content | Private rights of action + statutory damages |

| State Consumer Protection Acts | AI washing/misrepresentation | Treble damages + attorneys’ fees |

The private right of action is particularly significant. This means individuals can sue directly—they don’t need to wait for regulators to act. Class action attorneys are already mobilizing.

Product Liability’s AI Evolution

U.S. courts are increasingly treating AI chatbots and LLMs as “products” under traditional product liability theories. This is a seismic shift. Product liability imposes strict responsibility on manufacturers and distributors—you can be liable even without negligence if your product is defective and causes harm.

When AI becomes a “product,” every company deploying customer-facing AI inherits product liability exposure. Your chatbot gives bad medical advice? Product liability. Your recommendation engine discriminates? Product liability. Your content generator produces defamatory material? Product liability.

The Regulatory Fragmentation Problem

The IAIS Global Insurance Market Report 2025 flags AI adoption as a key supervisory priority, citing governance, transparency, bias, and operational risks. But here’s the complication: only 11 U.S. jurisdictions have issued AI guidance following the NAIC’s model bulletin.

This creates regulatory fragmentation that multiplies compliance costs. A company operating nationally must navigate a patchwork of requirements, with no harmonized federal framework to simplify compliance. Each state’s approach differs, creating gaps where liability exists but guidance doesn’t.

The D&O Exposure Nobody’s Discussing

Analysis of D&O liability implications reveals that directors and officers face personal exposure that most haven’t fully appreciated.

The Fiduciary Duty Question

Directors have fiduciary duties to oversee corporate risk management. When AI deployments create uninsured liabilities, boards face uncomfortable questions:

- Did the board understand the AI risks before approving deployment?

- Was there appropriate oversight of AI governance?

- Were shareholders adequately informed about AI-related risks?

- Did management implement reasonable controls?

Shareholder derivative suits alleging breach of fiduciary duty are already emerging. The “AI washing” class actions—those 50+ cases alleging misrepresentation of AI capabilities—often include D&O claims alongside securities fraud allegations.

The Disclosure Trap

Securities law requires disclosure of material risks. Is your AI liability exposure material? Almost certainly. Are your insurance coverage gaps material? Increasingly, yes. Have you disclosed them adequately? Most companies haven’t, because most companies haven’t fully assessed them.

This creates a disclosure trap: the more you understand your AI risks, the more you must disclose. The more you disclose, the more you acknowledge exposure you can’t insure. The more exposure you acknowledge, the more attractive a target you become for plaintiffs.

The Global Compliance Multiplier

For multinational organizations, the challenge compounds exponentially.

The EU AI Act became effective in December 2024, applying strict product liability to AI systems. European regulators are not waiting for harm—they’re imposing requirements before deployment. The Act’s tiered risk classification means high-risk AI systems face conformity assessments, documentation requirements, and ongoing monitoring obligations.

Analysis of AI ethics and workplace risks highlights how employment-related AI decisions—hiring, performance evaluation, termination—face particularly intense scrutiny under both EU and emerging U.S. frameworks.

Meanwhile, U.S. federal bills propose liability standards for both AI developers and deployers. The legislative trajectory is clear: liability is expanding, not contracting.

Companies operating globally face a compliance multiplication problem: EU requirements, varying U.S. state laws, emerging Asian frameworks, and sector-specific regulations all applying simultaneously to the same AI deployments.

Who Actually Bears Responsibility?

This is the question at the heart of the paradox: when AI causes harm, who pays?

The Vendor Liability Shell Game

Most companies deploying AI don’t build their own models. They use APIs, integrate foundation models, or license AI capabilities from vendors. Standard vendor agreements include limitation of liability clauses capping exposure at the contract value—often a fraction of potential damages.

When an AI system built on GPT-4, Claude, or Gemini causes harm, the liability flows downstream to the deployer, not upstream to the model provider. This is intentional. AI vendors have structured their terms of service to transfer risk to customers.

Insurance industry trend analysis notes that this liability structure creates a cascade effect: foundation model providers bear minimal risk, while deployers—often smaller companies with less sophisticated legal resources—absorb the exposure.

The Human-in-the-Loop Fiction

Many AI deployments claim “human oversight” as a liability shield. But this defense is increasingly hollow.

When AI systems process thousands of decisions per hour, human review becomes performative rather than substantive. The human-in-the-loop can’t meaningfully evaluate each AI output—they can only spot-check and hope. Courts and regulators are beginning to see through this fiction.

True human oversight requires:

- Sufficient time to evaluate each decision

- Technical understanding of how the AI reached its conclusion

- Authority to override AI recommendations

- Documentation of oversight activities

Most “human-in-the-loop” implementations satisfy none of these criteria. They’re liability theater, not genuine oversight.

The Corporate Accountability Illusion

Here’s the uncomfortable truth: we’ve created a system where AI harm can occur without clear accountability.

- Model providers disclaim liability in their terms of service

- Deployers can’t insure against AI-specific risks

- Human oversight is often nominal

- Regulatory frameworks are fragmented and lagging

- Courts are still developing AI liability doctrines

The result? When AI causes harm, the injured party may have no effective remedy. The harm is real, but the accountability is diffused across a chain of actors who each claim limited responsibility.

This is corporate accountability becoming an illusion—not through malice, but through structural gaps that no single actor has incentive to close.

What This Means for Your AI Strategy

If you’re a technology leader, board member, or risk manager, this analysis should fundamentally reshape your AI approach.

The Governance-Before-Deployment Imperative

The days of “move fast and break things” are over for AI. Not because of ethical considerations—though those matter—but because the insurance market is forcing the issue.

Market analysis makes clear that AI-specific insurance products are forming on insurers’ terms. Those terms require governance, documentation, and oversight. Companies that build these capabilities now will have access to coverage. Companies that don’t will be self-insuring against catastrophic risks.

The governance requirements aren’t optional nice-to-haves. They’re becoming prerequisites for operating AI at scale.

The True Cost Calculation

Most AI business cases don’t include liability exposure in their ROI calculations. This is financially negligent.

A realistic AI cost model must include:

- Insurance premiums for available coverage

- Self-insured retention for excluded risks

- Compliance costs across applicable jurisdictions

- Governance infrastructure investment

- Incident response and remediation reserves

- Legal defense costs for anticipated litigation

When you run these numbers honestly, many AI deployments look far less attractive. This doesn’t mean don’t deploy AI—it means deploy AI with eyes open about the true cost structure.

The Board-Level Conversation

Every corporate board should be asking:

- What AI systems are we deploying, and what risks do they create?

- What insurance coverage do we have for AI-related liabilities?

- What exclusions apply to our current policies?

- What governance frameworks do we need for insurability?

- What is our self-insured exposure for AI harms?

- How are we disclosing AI risks to shareholders?

If your board hasn’t had this conversation, you’re governing in the dark.

The Path Forward

This paradox won’t resolve itself. Insurance markets, regulatory frameworks, and corporate practices are all adjusting simultaneously, creating a period of genuine uncertainty. But some strategic principles are emerging.

Invest in Insurability

The companies that will thrive in this environment are those building toward insurability. This means:

Documentation: Every AI deployment needs comprehensive documentation of design decisions, risk assessments, and governance structures. This isn’t bureaucracy—it’s the foundation for insurance coverage and legal defense.

Testing: Bias testing, adversarial testing, and failure mode analysis must become standard practice. Insurers want to see that you’ve identified risks before deployment, not after harm occurs.

Oversight: Real human oversight, not performative checkbox compliance. This means staffing, training, and authority structures that enable meaningful review.

Incident Response: AI-specific incident response plans that address detection, containment, notification, and remediation. When—not if—something goes wrong, your response matters for both liability and insurability.

Rethink Vendor Relationships

Standard AI vendor agreements are designed to protect vendors, not customers. Companies need to negotiate for:

- Meaningful indemnification for model failures

- Transparency about training data and known limitations

- Contractual commitments on model behavior

- Audit rights for high-risk deployments

- Clear liability allocation for harm

Large customers have leverage. Use it. The alternative is accepting risk transfer on vendors’ terms.

Engage the Emerging Insurance Market

While standard coverage is shrinking, specialized AI insurance products are emerging. Early engagement with insurers helps in multiple ways:

- Understanding what governance requirements will be necessary

- Shaping product development to address your specific risks

- Establishing relationships before capacity becomes constrained

- Learning from insurers’ risk assessments of your operations

The $4.8 billion market projection represents real capacity coming online. Position yourself to access it.

Participate in Standard-Setting

The regulatory fragmentation—11 jurisdictions with guidance, 39 without—represents both risk and opportunity. Companies that engage constructively in standard-setting can help shape frameworks that are both protective and workable.

This isn’t about lobbying for weak regulation. It’s about ensuring that emerging frameworks are technically informed and practically implementable. Poorly designed regulation creates compliance burdens without meaningful risk reduction.

The Reckoning We Can’t Avoid

The AI liability insurance paradox forces a fundamental question: What does corporate accountability mean when risk cannot be transferred?

For decades, insurance functioned as a social mechanism for spreading harm across broad pools. When your product injured someone, insurance ensured compensation while allowing productive activity to continue. This system depended on risks being assessable, losses being uncorrelated, and moral hazard being manageable.

AI breaks these assumptions. The risks are not fully assessable. The losses can be highly correlated. The moral hazard is amplified by competitive pressure to deploy before governance catches up.

The insurance industry’s retreat from AI coverage isn’t market failure—it’s market honesty. They’re telling us the truth about AI risks that we’ve been avoiding: they’re real, they’re substantial, and they’re not someone else’s problem.

This means the “move fast” ethos must evolve. Speed without governance isn’t competitive advantage—it’s risk accumulation. Every AI deployment without appropriate controls creates potential liability that sits on your balance sheet, uninsured and growing.

The companies that recognize this earliest will have structural advantages. They’ll attract better insurance terms, face lower litigation risk, and build more sustainable AI practices. The companies that don’t will discover the hard way that liability deferred is liability multiplied.

We’re entering an era where AI accountability cannot be outsourced. Not to insurers, not to vendors, not to the fiction of human oversight. The responsibility stays with the organizations deploying AI and the leaders approving those deployments.

This is uncomfortable. It’s also correct. AI is too powerful and too unpredictable to operate on the assumption that someone else will clean up the mess. The insurance industry figured this out first. The rest of us are catching up.

The era of deploying AI now and figuring out accountability later is ending—companies that don’t build governance before deployment will find themselves competing with uninsurable balance sheets against organizations that understood the paradox before it became their crisis.